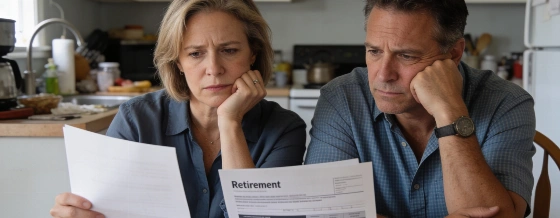

A new survey finds 62% of Americans worry they'll reach retirement age without enough savings, as concerns mount over Social Security cuts, rising living costs, and the high price of long-term care

More Americans are questioning whether their retirement savings will be enough, even if they work until traditional retirement age. According to a recent survey by the Transamerica Center for Retirement Studies, 62% of respondents said they believe they could reach retirement and still fall short financially. This widespread anxiety reflects a mix of economic pressures, policy uncertainty, and shifting expectations about what retirement will actually look like for millions of U.S. households.

Several factors are fueling these concerns. Persistent inflation has eroded the purchasing power of savings, while the cost of essentials-from housing to healthcare-continues to climb. Many workers are also watching the future of Social Security with unease. The latest Social Security Trustees Report projects that the Old-Age and Survivors Insurance Trust Fund will be able to pay full benefits only until 2033. After that, unless Congress acts, beneficiaries could see their payments reduced to about 77% of the amounts currently promised. For those relying on Social Security as a primary income source, even a partial cut could significantly impact their standard of living.

Healthcare and long-term care costs are another major source of anxiety. As people live longer, the likelihood of needing extended care increases, but the price of long-term care insurance has risen sharply. Policies purchased at a younger age typically come with lower premiums, but buyers may end up paying for decades before ever making a claim. Financial planners often suggest that individuals start evaluating long-term care insurance options in their early 50s, when coverage is more accessible and health issues are less likely to disqualify applicants. Still, the decision involves weighing high ongoing costs against the risk of facing even larger out-of-pocket expenses later in life.

For those worried about a retirement savings gap, experts recommend a clear-eyed assessment of current assets, projected expenses, and potential shortfalls. This means tallying up all retirement accounts, estimating future income sources, and comparing them to realistic spending needs. If a gap exists, increasing contributions to tax-advantaged accounts like 401(k)s and IRAs can help, especially if an employer offers a matching contribution. Reducing discretionary spending-such as dining out or subscription services-may also free up cash for savings. For those eligible, a Roth IRA offers tax-free withdrawals in retirement, but annual contribution limits and income thresholds apply.

According to the Federal Reserve's 2023 Survey of Household Economics and Decisionmaking, only 31% of non-retired adults said their retirement savings were on track, while 36% felt they were significantly behind. The same report found that nearly half of adults expect Social Security to be a major source of income in retirement, underscoring the potential impact of any benefit reductions. Meanwhile, the median retirement account balance for working-age households remains well below what most experts consider sufficient for a comfortable retirement.

While there is no one-size-fits-all solution, the combination of rising costs, uncertain benefits, and longer lifespans means that many Americans will need to revisit their retirement plans more frequently. This may involve adjusting savings rates, rethinking investment strategies, or even considering part-time work in retirement to bridge the gap. For those facing complex decisions about insurance, taxes, or investment allocations, consulting a qualified financial professional can help clarify options and trade-offs.

Long-term care insurance is a specialized product designed to cover services that regular health insurance and Medicare typically do not, such as assistance with daily living activities in a nursing home or at home. Premiums can vary widely based on age, health, and coverage features, and policies often include waiting periods and benefit caps. Unlike life insurance, long-term care coverage is not guaranteed to pay out, and premiums can increase over time. Understanding the fine print, including exclusions and inflation protection options, is essential before committing to a policy. As with all major financial decisions, comparing multiple providers and seeking unbiased advice can help consumers avoid costly mistakes.